Making Money Matters Easier: Personal Loans Unveiled

As the world of personal finance continuously unfolds, the ease and approachability of an immediate loan have surfaced as a ray of hope for numerous individuals. Be it unexpected fiscal challenges or seizing an opportunity, many consider these types of accommodations their go-to choice. Offering flexible conditions, appealing rates on interest, and a simple application procedure - such borrowings largely mitigate financial stress experienced by countless persons worldwide. Allow us to explore in-depth how utilizing this kind of financing can become part & parcel of your economic arsenal.

The Convenience Factor:

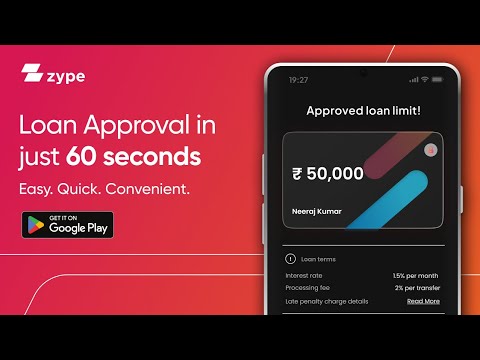

Unpredicted obstacles frequently crop up in life, putting a stranglehold on our financial situation. This could be an unexpected healthcare cost, unplanned maintenance work, or even educational endeavors - instances where fast approved loans offer the vital fiscal lifeline we need during emergencies. Their speedy and trouble-free application method makes these credits a dependable solution when other options are seemingly out of reach.

Flexibility in Repayment:

The fast online loans distinctively shine in their adaptable payment structure. Considering the differing financial conditions prevalent among individuals, such loans offer modifiable repayment choices that can be finely adjusted to cater explicitly to individual requirements. Such a trait not only fortifies economic stability but also allows borrowers the freedom to strategize their repayments well-aligned with specific monetary situations.

Competitive Interest Rates:

In the sphere of individual budgeting, interest rates maintain a crucial position in fast loan online assessing the feasibility of loan choices. Private loans celebrated for their attractive interest figures boost customers to chase down their economic ambitions minus any fears about excessive reimbursement quantities. Furnished with moderate lending terms, clients are able to boldly navigate through fiscal ventures without barriers posed by formidable debt commitments.

Streamlined Application Process:

The era of tiresome form-filling and lengthened delays is over. The modernized method for personal loans has radically changed how people obtain monetary aid. Equipped with fewer paperwork requirements and effective online platforms, interested individuals can now submit their loan applications from within their own dwellings--a move that conserves time and vigor alike. This slick procedure guarantees financial help at one's disposal when it becomes necessary, sidestepping superfluous red tape.

Empowering Financial Stability:

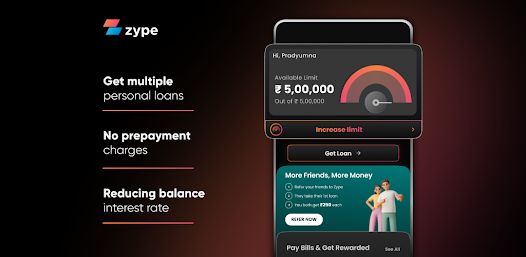

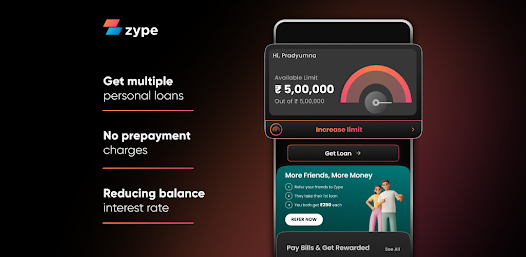

Personal loans provide more than just a momentary fix to financial pressures; they serve as facilitators of sustained economic solidity over time. Be it amalgamating pre-existing debt, investing in knowledge advancement, or initiating business ventures, such a flexi personal loan bestows people with the ability to make forward-thinking fiscal choices that lay grounds for prospective progress and achievement. They offer an entrance into funding sources that may have previously been unattainable, thereby acting as key unlocking substantial opportunities capable of transforming one's monetary direction.

Wrapping Up:

In the sphere of individual monetary affairs, access to private loans has revolutionized one's approach toward fiscal hurdles. Thanks to their uncomplicated procedures, adaptable conditions, and appealing rates, these borrowings have showcased immense value in easing financial pressure while paving a path for an economically healthier future. By grasping subtleties and advantages linked with personal loans, individuals can leverage their potentiality, steering smoothly through intricate aspects of life's finances confidently & effortlessly. Have faith as economic liberation is nearer than you think. Plus, personal lending could be your bridge leading to a wealthier and more stable forthcoming day.